State Farm filed for a 17.9% overall rate increase on its California Business Risk Types line, effective September 15, 2026, for both new and renewal business.

The filing reflects a sharp divergence between coverages, with property rates decreasing by 14.3% while liability rates increase by 83.3%.

The primary driver is continued pressure on liability losses. State Farm points to social inflation, rising litigation costs, and larger jury awards as key factors increasing claim severity. While property trends have stabilized due to easing economic inflation, liability costs continue to escalate. The company also highlights the growing role of third party litigation financing, which is contributing to higher claim costs and a more active legal environment.

The California businessowners book is sizable at roughly $423 million in annual premium, with about $283.6 million in property and $139.7 million in liability. The portfolio includes approximately 90,575 policies, with an average premium of around $4,700 per risk.

Performance varies significantly across segments. Property remains profitable with a loss ratio near 52%, while liability is deeply unprofitable at roughly 116%, reinforcing the need for outsized rate increases on that side of the book.

The portfolio has also been shrinking. State Farm reports a 25% decline in exposures over the past two years, driven by cancellations and its decision to stop writing new business in May 2023.

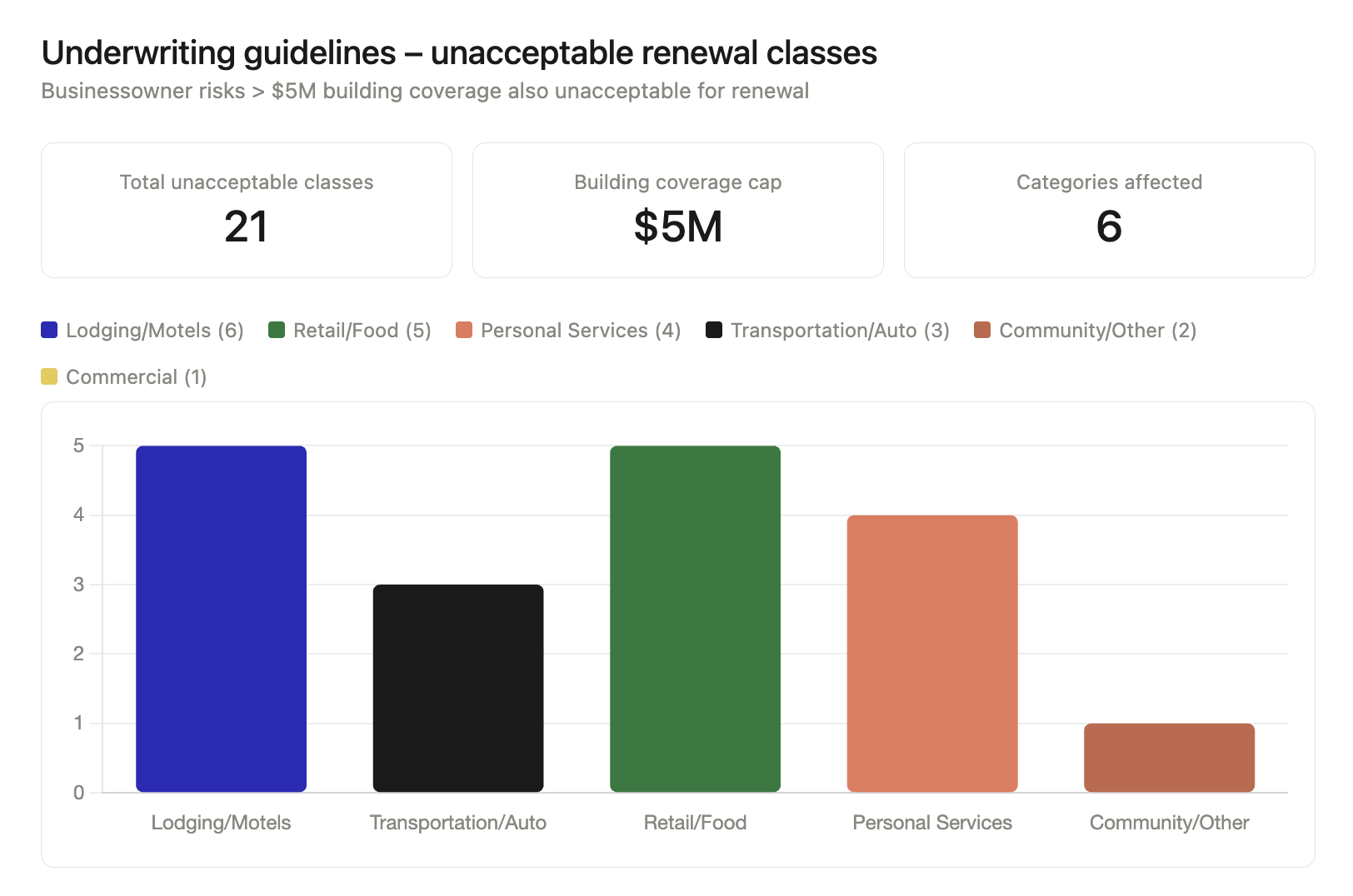

Beyond pricing, the filing introduces tighter underwriting. The company plans to nonrenew several higher risk classes, including motels, convenience stores, and certain service businesses, and will no longer accept risks with building coverage above $5 million.

Overall, the filing underscores a clear shift in commercial lines dynamics: liability is deteriorating and driving rate need, while property remains stable and profitable.